The human face of a health reform debate

McConnell-Grimes debate reveals clearly what’s at stake in Kentucky; reaction from blog readers puts health reform debate in human terms

A few days ago I posted a widely read deconstruction of the baker's dozen lies Mitch McConnell told about the Affordable Care Act in his debate with Alison Lundergan Grimes (plus another dozen or so confusing or downright bizarre points which came up during the five-minute exchange with the moderator).

The major standouts were:

- The Kynect exchange is far more than "just a website" ... with no better proof than the fact that Oregon managed to enroll a similar number of people (about a half a million) in healthcare coverage without a working exchange website. I'm not saying they should be proud of having to do it that way, but the point is that the website is merely a means of achieving the real point of the ACA exchanges: Enrolling as many people as possible in affordable healthcare plans.

- No, you can't repeal "Obamacare" without also repealing "Kynect," because the latter only exists as long as the former does. Yes, it's theoretically possible that you could repeal the ACA and then bring Kynect back ... but in order to do so, you'd have to jack up the tax rate on Kentucky citizens to the tune of $700 million or more.

- The CBO never said anything about 2.5 million jobs being lost, and $716 billion would be saved for Medicare over a decade, not "cut."

... and so on.

I stand behind everything I said, but let's face it, most of what I write is number-crunchy bean counting. What's far more important is what the law means for actual people. The human factor can't be underscored enough.

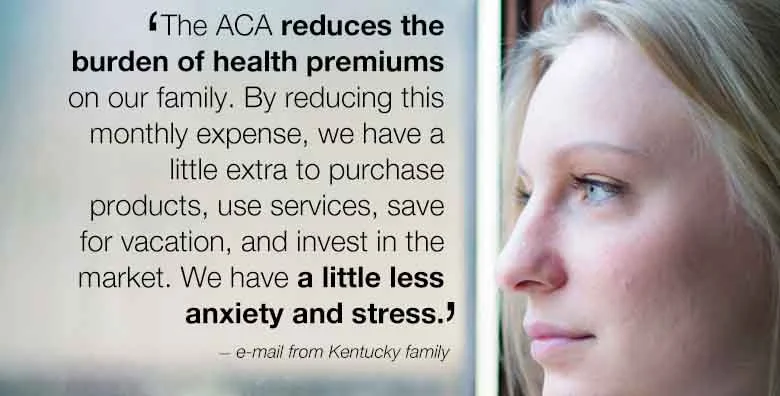

'A little less anxiety and stress month to month'

Fortunately, the very next day, I received an e-mail from a Kentucky resident who expressed the reality of the situation there far more eloquently than I did. Here's a snippet:

I invite you to read the whole thing.

I immediately asked him if I could post the letter publicly, and he explained that sure, that was kind of the point: To get the word out about what the ACA means to him and his family in Kentucky ... and what a shame it would be to see Mitch McConnell and his cronies have a chance of taking it all away again.

The cold, hard economics of Medicaid

The following day I received another e-mail from a Kentucky resident ... a self-declared Republican. He first noted that 80 percent of the residents of his county are on Medicaid. (I'm not sure if that was before or after ACA expansion.) But then her returned to the other side of the equation: cold, hard economics.

To his credit, he was polite, respectful, thoughtful and he raised a fair point:

Again, read the whole letter; I was genuinely moved by what he had to say, no snark.

My response:

The following is my response to the second letter. (I responded to the writer by e-mail, but I'm posting the response here for the first time.)

- CORRECTION: It's been brought to my attention that the states are NOT responsible for any more than 10% of the cost of expanded Medicaid even after 2022: Under the health-care law, the federal government will pay 100 percent of the cost of expansion in 2014, 2015 and 2016. Then the federal match is pared back to 95 percent in 2017, 94 percent in 2018, 93 percent in 2019 and then 90 percent in 2020 and beyond. It would stay at the 90 percent level unless the lawmakers change or repeal the legislation.)

(CORRECTION: Again, see my note above.)