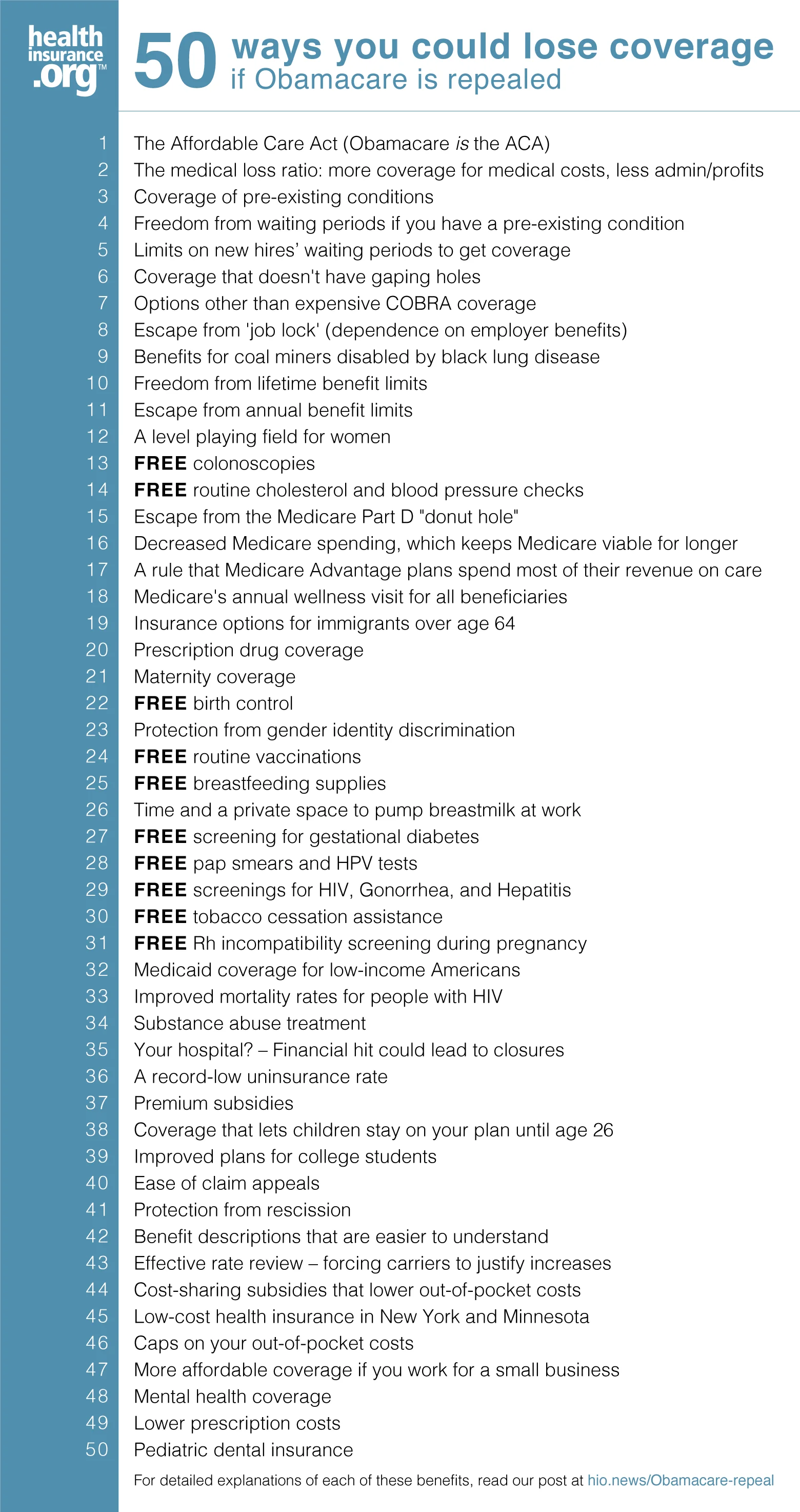

Download the infographic 50 ways you could lose coverage if Obamacare is repealed

After nearly a decade of railing against the ACA, Republican lawmakers spent much of the first year of President Trump’s administration trying to pass legislation to repeal significant portions of the law. They were unsuccessful, however, and subsequently lost their majority in the House — leaving the ACA fairly safe from legislative attacks for the time being.

But the Trump administration issued numerous regulations designed to chip away at the law, including rules to expand short-term health insurance plans and association health plans, and terminated federal funding for cost-sharing reductions in late 2017. The administration has also reduced funding for exchange marketing and enrollment assistance over the last few years.

Yet the ACA has survived. Enrollment in plans sold through the exchanges is down about 10 percent from the high it reached in 2016, but premiums have stabilized in 2019 and 2020, and insurer participation in the exchanges has been growing for the last two years.

But the ACA’s future still hangs in the balance in 2019, this time via the Texas v. Azar court case. The ACA already survived a landmark court challenge in its early years, when the Supreme Court upheld most of the law but made Medicaid expansion optional (there are still 14 states that have taken no action to expand Medicaid). But Texas v. Azar could topple the law, with a ruling by the 5th Circuit Court of Appeals expected as soon as October 2019.

Texas v. Azar actually hinges on the Supreme Court’s 2012 ruling that upheld the constitutionality of the ACA: The justices ruled at that point that the ACA’s individual mandate included a tax, rather than a penalty, for non-compliance. But that tax was repealed, effective January 1, 2019, by the Tax Cuts and Jobs Act that was enacted in late 2017.

Plaintiffs in the Texas v. Azar case include 20 GOP-led states. They are arguing that since the tax for non-compliance with the individual mandate no longer exists, the ACA itself should be overturned. Although that seems like a far-fetched interpretation, a federal district court sided with the plaintiffs in December 2018, striking down the entire ACA.

The case was appealed, and the ACA has remained intact throughout the litigation process. But the US Department of Justice is not defending the ACA. Instead, Democratic-led states have taken on that responsibility. The Fifth Circuit Court of Appeals heard oral arguments in the case in the summer of 2019, and a ruling is expected in the fall of 2019.

Quite a few states –– have implemented their own laws to protect consumers in the event that the ACA is overturned. But without the federal funding that covers the cost of premium subsidies and Medicaid expansion, it’s doubtful that very many states could uphold the same level of consumer protections that people currently receive under the ACA.

To be clear, nothing will change overnight, even if the appeals court upholds the lower court’s decision to invalidate the ACA; the appeals process is likely to continue all the way to the Supreme Court. But the timing of a decision against the ACA could certainly be problematic: If headlines proclaim that the law has been overturned shortly before or during open enrollment for 2020 coverage, it could result in widespread confusion among consumers, especially those who obtain their health insurance in the individual market.

But that’s really not very many people. Only about 7 percent of Americans get their health insurance in the individual market, and that’s where the bulk of the ACA-related headlines have focused over the last several years.

So does the rest of the country need to worry about the ACA being overturned? Absolutely, yes. But unfortunately, the average American may not have a good sense of what they stand to lose if the ACA is overturned. Many aren’t even certain that they’ve gained anything from the law. So to clarify, I’ve created a list of 50 things we’d lose if Obamacare were to be overturned in the court system (And I choseIf Republican-led states and the Trump administration succeed in their efforts to overturn Obamacare, here’s what they’d be taking away:

- The Affordable Care Act. In case you had any doubt, Obamacare is just another name for the Affordable Care Act (though more than a third of Americans don’t know that).

- The medical loss ratio. It’s the mandate that says health insurance companies have to spend the majority of their members’ premiums on medical costs.

- Coverage of pre-existing conditions. Before the ACA, people with pre-existing conditions found it expensive or impossible to get coverage in the individual market.

- … and freedom from waiting periods if you have a pre-existing condition. The ACA eliminated the waiting periods that employer-sponsored health plans used to impose before covering pre-existing conditions.

- Limits on waiting periods. If you get a new job and you’re eligible for your employer’s health plan, you might have to again wait more than 90 days before your coverage begins. The ACA limited waiting periods for newly eligible employees to no more than 90 days.

- Coverage that doesn’t have gaping holes. Employers could also go back to offering “mini-meds” and plans with huge holes in the coverage. Remember the movie John Q? Do you want the possibility that your employer might put you on a health plan that doesn’t cover organ transplants? Or that limits your total benefits to $10,000 a year? Or $2,000? The only reason large employers aren’t offering those plans anymore is because the ACA penalizes employers if the coverage they offer doesn’t meet minimum value standards. Without the ACA, those plans would return.

- Freedom from expensive COBRA coverage. People with pre-existing conditions who want to leave a job to become self-employed will likely find that COBRA coverage with budget-crushing premiums is once again their best option. (And COBRA isn’t available for all job-sponsored health plans).

- Escape from ‘job lock.’ In general, people will find themselves much more limited in their career options. Entrepreneurial paths will be unavailable to many, because the well-regulated individual market will revert to the “Wild West” system that existed pre-ACA.

- Benefits for coal miners and their survivors. Miners disabled by black lung disease, and their survivors, are eligible for federal benefits as a result of Section 1556 of the ACA, but could lose them if the ACA is overturned.

- Freedom from lifetime limits. Lifetime benefit limits will come back. If you or a loved one has hemophilia or a very premature baby, for example, you could use up all of your health insurance benefits very quickly, and have nowhere else to turn.

- Escape from annual benefit limits, which are similar to lifetime limits, only smaller.

- A level playing field for women. It’s likely that women will again charged more for coverage than men – like they were in the “good old days” –.

- FREE colonoscopies. A colonoscopy can cost more than $2,000 if you have to pay for it yourself.

- FREE routine cholesterol and blood pressure checks will no longer be free.

- Escape from the Medicare Part D “donut hole.” The donut hole will be back with a vengeance. Before the ACA, Medicare enrollees had to pay the full cost of their medications while they were in the donut hole. In 2020, seniors don’t have to pay more than 25 percent of the cost of their medications while in the donut hole. Without the ACA, they’ll be back to paying 100 percent.

- Decreased Medicare spending. Without the ACA, Medicare spending is projected to increase by $802 billion over the next decade. The result will be higher premiums, copays, deductibles and coinsurance for Medicare beneficiaries.

- The requirement that Medicare Advantage plans spend most of their revenue on members’ care. Under the ACA, Medicare Advantage plans have to spend no more than 15 percent of revenue on administrative costs; at least 85 percent has to be spent on medical care and quality improvements or else the health plan has to send money back to CMS and eventually stop enrolling new members. Without the ACA, that requirement would no longer exist.

- Medicare’s annual wellness visit for all beneficiaries. It’s available now as a result of the ACA, but would disappear if the ACA is overturned.

- Insurance options for immigrant over age 64. Do you have elderly parents living overseas, who would like to move to the U.S.? If the ACA is overturned, they’ll have little in the way of health insurance options for the first five years after they move here. They can’t buy into Medicare during that time, and would be declined by individual market health plans if pre-ACA rules are resurrected. (Individual market plans used to reject enrollments from people over the age of 64, even if they weren’t eligible for Medicare.)

- Prescription drug coverage. Before the ACA, there was a trend in the individual market towards health plans that didn’t include prescription drugs or that only covered generics. Medications are expensive, and not covering them was a good way to hold down costs and keep premiums low. That might sound fine – until you actually get sick and need prescriptions. For example, there aren’t any MS drugs that cost less than $50,000/year, which is a bit of a stretch if your health plan doesn’t cover medications.

- Maternity care. Most health plans in the individual market won’t cover maternity care if the ACA is overturned. In many states, you won’t haveoptions for plans with maternity coverage if you don’t have access to an employer-sponsored plan.

- FREE birth control. Free contraception will disappear. IUDs will go back to costing $500 to $1,000 upfront, and female sterilization will set you back up to $6,000. (Both are covered in full under Obamacare).

- Protection from discrimination. LGBT Americans will likely lose access to coverage and necessary medical treatment. Section 1557 of the ACA prohibits discrimination in health plans, including discrimination based on gender identity or sexual orientation. That has been a boon to the LGBT community, but without the ACA’s protections, many would find their access to health care in jeopardy once again.

- FREE routine vaccinations. You’ll have to start paying for them again – including fees for the office visit and the vaccine itself.

- FREE breastfeeding supplies. New moms will no longer have access to free breastfeeding supplies (such as a pump) and the support they need to successfully breastfeed.

- Privacy if you’re breastfeeding. Nursing mothers might no longer have realistic access to pumping milk while at work. ACA Section 4207 requires large employers to provide nursing mothers with a private space (not a bathroom) in which they can pump, and adequate time to do so during the workday. If you know a nursing mother, she’s grateful for this provision.

- FREE screening for gestational diabetes will disappear, and pregnant women will have to pay for the screening (along with the full cost of their maternity care if they have coverage in the individual market).

- FREE pap smears and HPV tests. Obamacare requires insurers to provide free pap smears and HPV tests, but if the law is overturned, expect to start paying for those again, including office visit copays and lab charges.

- FREE screenings for HIV, Gonorrhea, and Hepatitis. These screenings are part of the ACA’s preventive care requirements.

- FREE tobacco cessation. Under Obamacare, health insurance plans provide cessation assistance. If the law is overturned, you’ll pay for that again too.

- FREE Rh incompatibility screening. The ACA requires free Rh incompatibility screening for pregnant women, which can be lifesaving for the baby.

- Medicaid coverage for low-income Americans. Millions who’ve relied on Medicaid since 2014 could find themselves uninsured again. Obamacare expanded Medicaid, but the Supreme Court made it optional for states. As of 2019, Medicaid has been expanded in 34 states and DC with two more states in the process of implementing Medicaid expansion. Total enrollment in Medicaid/CHIP has increased by 15.6 million people since 2013. Louisiana expanded Medicaid in 2016, and has been maintaining a website that shows the number of people who have obtained preventive care and potentially life-saving treatment as a result. It’s eye-opening, especially when you consider the same impact in 33 other states, most of which expanded Medicaid more than two years before Louisiana.

- Improved mortality rates for people with HIV. Under Obamacare, people with HIV are less likely to die since ACA-compliant coverage is guaranteed-issue and the majority of the states have expanded Medicaid. Eliminating the ACA would reverse the declining trend in mortality rates.

- Substance abuse treatment. Without the ACA, individual and small-group plans will no longer be required to cover substance abuse treatment. Millions of people on Medicaid will also lose their coverage that includes benefits for substance abuse treatment. That’s not likely to help combat the current opioid crisis.

- Your hospital? It could happen. Some hospitals – particularly in rural areas – will close, particularly in the states that accepted the ACA’s Medicaid expansion – and thus significantly decreased their uninsured rates since 2013. If low-income populations in those states revert to being uninsured, hospitals will still have to treat them in emergency situations, but will receive little or no compensation for doing so.

- Our current uninsured rate. After decreasing steadily since 2013, the percentage of uninsured Americans began to creep upward under the Trump administration. But if the ACA is overturned, it will spike drastically higher. In 2017, when ACA repeal was being debated in Congress, the Congressional Budget Office estimated that the number of uninsured Americans would increase by 32 million over the coming decade if the ACA were to be overturned.

- Premium subsidies. Middle-class Americans who buy their own health insurance will lose the subsidies (tax credits) that currently pay the majority of their premiums. Eighty-seven percent of exchange enrollees nationwide are receiving premium subsidies in 2019, and the subsidies average more than $500/month.

- Coverage on your plan for your adult children. Young adults will no longer be able to stay on their parents’ health insurance plans until age 26.

- Improved plans for college students. Thanks to the ACA, the health plans offered to college students today are just as good as the plans offered to everyone else. If the law is overturned, health plans offered to college students will revert to limited-benefit coverage with low annual benefit maximums.

- Ease of claim appeals. Under Obamacare, there’s an internal appeals process, and if that doesn’t work, you have the right to an external review by an independent organization. Those protections would disappear without Obamacare.

- Protection from rescission. Under the ACA, recission (retroactive cancellation of your coverage) by your health insurance carrier is prohibited – unless your application was fraudulent or included intentional misrepresentation. Back in the pre-ACA days, in most states, individual health insurance applications included numerous questions about the applicant’s medical history. If an applicant forgot to mention a condition, and then later developed a completely unrelated medical condition, the carrier could rescind the policy based on the application error. The rules about rescission are more stringent under Obamacare, but more to the point, health insurance applications no longer ask about medical history (other than tobacco use), which eliminates much of the misrepresentation problems that used to occur.

- Easier to understand benefit descriptions. The ACA requires health insurers to provide coverage explanations in easy-to-understand, standardized formats, along with uniform definitions of health insurance terminology. Without the ACA, that standardization and simplification would no longer be required.

- Effective rate review. Before the ACA was implemented, some states went to great lengths to ensure that premiums were actuarially justified, but others did very little. Combined with the fact that there were no federal medical loss ratio requirements in place before the ACA, residents in some states were getting fleeced by some health insurers. The ACA implemented a system that requires an actuarial review of any proposed rate increase of 10 percent or more (a threshold that has since been raised to 15 percent), and details are published so consumers can see them. Without the ACA, rate reviews would become essentially meaningless in some states.

- Cost-sharing subsidies that lower out-of-pocket costs. Despite the fact that the Trump administration terminated federal funding for cost-sharing reductions (CSR) in 2017, the benefits continue to be available to eligible enrollees, keeping out-of-pocket medical costs much lower than they would otherwise be. If you earn $20,000 a year and you’ve got a health plan through the exchange that has no deductible, you’re benefitting from the ACA’s cost-sharing subsidies. Without them, health care would become much less affordable.

- Low-cost health insurance in New York and Minnesota. If you’re in New York or Minnesota and you earn too much for Medicaid eligibility, but not more than 200 percent of the poverty level, you’re currently eligible for Basic Health Program coverage. In New York, it’s called the Essential Plan, and in Minnesota, it’s called MinnesotaCare. These programs were established under Section 1331 of the ACA – and will be eliminated if the ACA is overturned.

- Caps on your out-of-pocket costs. Under the ACA, health plans have to cap enrollees’ out-of-pocket exposure for in-network care. In 2020, the upper limit is $8,150 for an individual, and $16,300 for a family (many plans have limits well below that, but that’s the maximum). And the individual limit is required to be embedded in family plans. Without the ACA, we’d see a return of plans that have out-of-pocket limits of $20,000 or more. Those plans were particularly problematic when they were marketed to lower-income people, especially if the out-of-pocket exposure wasn’t well explained in the marketing materials and presentation.

- More affordable coverage if you work for a small business. Do you work for a small business that’s providing you with health insurance? Your employer might be getting an ACA-created tax credit to make offering coverage more affordable. If the ACA goes, small-business tax credits for health insurance premiums would disappear, too.

- Mental health coverage. Pre-ACA, more than a third of individual market health plans did not include coverage for mental health care. But it’s one of the ACA’s essential health benefits, which means it’s now included on all individual and small group health plans that have taken effect since 2014. Without the ACA, insurers could revert to plans that have minimal or no mental health coverage.

- Lower prescription costs. Low-income seniors and disabled Americans could see increased prescription costs. Section 3309 of the ACA eliminated out-of-pocket drug costs for people who are covered by both Medicare and Medicaid, if they are receiving home-based care that allows them to avoid having to move into a nursing home. People who are dual-eligible for Medicare and Medicaid are among our most vulnerable populations.

- Pediatric dental insurance. Do your kids have dental insurance now? Pediatric dental coverage is one of the ACA’s essential health benefits, and the percentage of children with dental coverage is at an all-time high.

Did any of these benefits catch you by surprise? If so, you’re not alone. It’s common for people to think that Obamacare only encompasses the health insurance exchanges, or that its provisions only apply to a small segment of the American population. In reality, that couldn’t be further from the truth.

It’s true that the ACA has flaws, and could use some fine-tuning. But losing it would eliminate a multitude of positive changes that have been implemented over the last several years.